%20(1).jpg?width=264&height=160&name=Website%20Featured%20Content%20Images%20(2)%20(1).jpg)

%20(1).jpg?width=300&height=175&name=Mega%20Menu%20Image%20(2)%20(1).jpg)

%20(1)-Mar-08-2024-09-27-14-7268-PM.jpg?width=300&height=175&name=Untitled%20design%20(6)%20(1)-Mar-08-2024-09-27-14-7268-PM.jpg)

%20(1)-1.jpg?width=264&height=160&name=Website%20Featured%20Content%20Images%20(2)%20(1)-1.jpg)

-1.jpg?width=264&height=160&name=Website%20Featured%20Content%20Images%20(1)-1.jpg)

%20(1).jpg?width=264&height=160&name=Website%20Featured%20Content%20Images%20(3)%20(1).jpg)

%20(1).jpg?width=264&height=160&name=Website%20Featured%20Content%20Images%20(4)%20(1).jpg)

-Mar-08-2024-08-50-35-9527-PM.png?width=300&height=175&name=Untitled%20design%20(1)-Mar-08-2024-08-50-35-9527-PM.png)

.jpg)

Recent News & Insights

QuickBooks

QuickBooks Online Checklist

Is QuickBooks Online right for you? QuickBooks Online can help you better manage your business ...

Accounting

What You Need to Know About the IRS’s CP53E Notices

The IRS has begun issuing CP53E Notices following a recent executive order directing federal ...

Manufacturing

Data-Driven Inventory Management: Using Power BI to Optimize Cash Flow & Financing

Inventory is one of the largest uses of cash for many businesses, yet it’s often managed with ...

Recent News

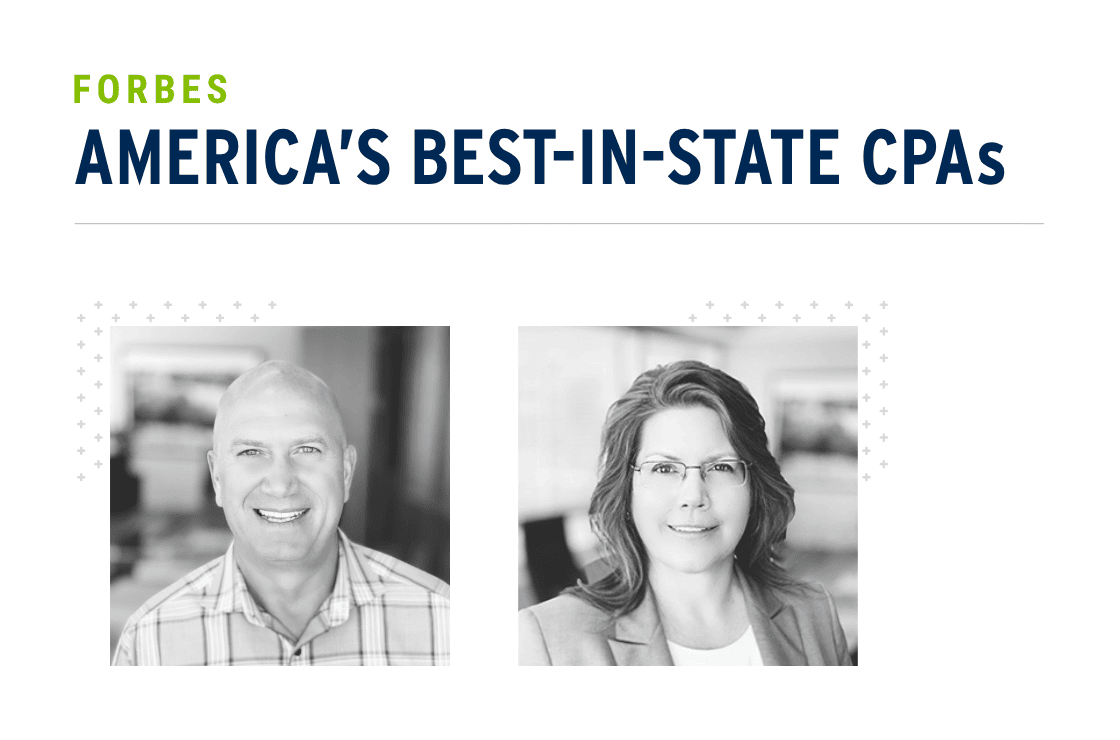

Duren & Martinson Named Forbes 2026 Best‑in‑State CPAs

Lutz is proud to announce that Mark Duren and Kelly Martinson have been named to the 2026 ...

Let’s get you where you want to go.

We work to simplify complexities, help make critical business decisions, and confidently focus on the things that are truly important to you. We embrace your business as our own to spark the right solutions and help you thrive.