.jpg?width=300&height=175&name=Mega%20Menu%20Image%20(1).jpg)

%20(1).jpg?width=300&height=175&name=Mega%20Menu%20Image%20(2)%20(1).jpg)

%20(1)-Mar-08-2024-09-27-14-7268-PM.jpg?width=300&height=175&name=Untitled%20design%20(6)%20(1)-Mar-08-2024-09-27-14-7268-PM.jpg)

%20(1)-Mar-08-2024-09-11-30-0067-PM.jpg?width=300&height=175&name=Untitled%20design%20(3)%20(1)-Mar-08-2024-09-11-30-0067-PM.jpg)

%20(1).jpg?width=300&height=175&name=Mega%20Menu%20Image%20(3)%20(1).jpg)

%20(1).jpg?width=300&height=175&name=Mega%20Menu%20Image%20(4)%20(1).jpg)

%20(1).jpg?width=300&height=175&name=Mega%20Menu%20Image%20(5)%20(1).jpg)

-Mar-08-2024-08-50-35-9527-PM.png?width=300&height=175&name=Untitled%20design%20(1)-Mar-08-2024-08-50-35-9527-PM.png)

.jpg)

In recent weeks the financial markets have displayed a traditional warning sign that has garnered significant attention. Widely viewed as one of the most reliable and accurate predictors of an economic slowdown, this signal has intensified the debate on where we are at in the economy. I am referring to, of course, the inversion of the yield curve. If you follow the financial media, you have most likely been exposed to some of these deliberations. What follows is a primer on what the yield curve is, some perspective on what an inversion has meant in the past, and whether investors should care.

Yield Curve 101

The yield curve is a graphical representation of yields for bonds with varying maturities ranging from short to long-term. The curve is typically associated with Treasury bonds, and it provides investors with a visualization of risk (time to maturity) and reward (yield) in the market. As the long-term average line in the chart below illustrates, yield has historically increased with time to maturity. This is generally because an investor will require more reward for bearing extra risk. The longer the period you have your money tied up, the larger the chance something could go awry. When the yield curve slopes upward, it is considered “normal”, and signifies the presence of the risk (term) premium.

Source: Treasury.gov. Long-term average calculated using daily yields from 1/2/1990 – 3/29/2019

Investors monitor the slope over time by comparing long-term yields with short-term yields. An inversion occurs when the long-term yield falls below that of the short. The spread between the 10-year Treasury bond and 3-month Treasury bill is among the most followed, and in late March it inverted for a couple of days.

Short-term interest rates are generally driven by monetary policy established by the Federal Reserve, while long-term rates are arguably driven by market expectations for economic growth and inflation. When the curve inverts, it can be interpreted as the market’s expectation for weaker growth in the future. The blue line above reflects the yield curve as of the end of March, with an apparent slight downward slope.

A Crystal Ball?

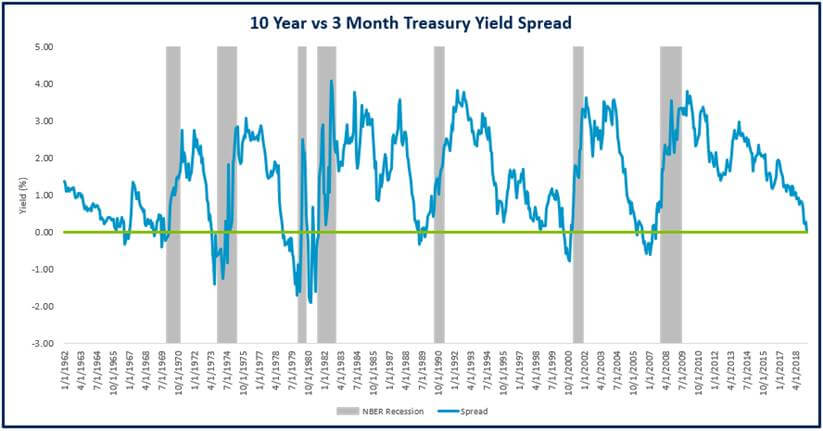

People pay close attention to the yield curve, because of its track record as an accurate forecaster of upcoming recessions. The yield curve has inverted ahead of all seven recessions endured by the U.S. economy going back over 50 years, while flashing a false positive just once. You would be hard pressed to find another indicator with that much success.

The chart below illustrates the historical experience. The blue line represents the monthly spread between the 10-year Treasury bond and 3-month Treasury bill yields going back to the early 1960’s. You can see that ahead of every recession (highlighted by the grey bars), the curve has inverted. The lone false positive occurred in the mid-1960’s.

As accurate as the signal has been historically, acting on it presents significant challenges. One of the primary drawbacks has been the considerable variability in the timing between the inversion and the onset of the recession. Going back to the 1960’s the time lag has ranged anywhere from 6 to 23 months (Average: 13 months).

Source: Fred.stlouisFed.org. Data as of 1/31/1962 – 3/29/2019. The 10-year yield is represented by the 10-Year Treasury Constant Maturity Rate. The 3-month bill is represented by the 3-Month Treasury Bill Secondary Market Rate until 1/4/1982, and the 3-month Treasury constant maturity rate thereafter. The spread was calculated on the last trading day of each month. Recessions represented by the NBER monthly peak through trough index.

Another issue relates to equity market performance following the inversion. You would generally expect stocks to decline if you had a strong reason to believe the economy was on a path to recession, but this hasn’t been the case historically. Following the last 8 inversions, U.S. stocks were positive on average 3 to 12 months later. Any investor that sold out immediately following the signal would have missed out on those gains. Additionally, the overall range of return outcomes (displayed in the table below as the Max-Min Spread) is extremely wide. For example, while the average 12-month return following an inversion was a pedestrian 5.10%, past returns were as high as +30.59% and as low as -14.49%. A market timing signal that keeps you within a 45% range is not particularly useful.

Source: Morningstar Direct. Data as of 1/31/1962 - 3/29/2019. Equity Returns are based on monthly IA SBBI Large Cap Stock Index data, and begin the first day of the month following the initial inversion. Returns for periods in excess of 12 months are annualized.

Despite the impressive accuracy inversions have displayed in predicting recessions, many market participants are not buying it. There are a variety of explanations for why an inverted curve may have lost its predictive power. Among the most frequently cited is that quantitative easing, an unconventional policy tool used by the Federal Reserve in the wake of the financial crisis, has artificially suppressed long-term rates. Others point to the fact that the curve, defined as the spread between 10-year bonds and 3-month bills, only remained inverted for a couple of days. Finally, the relative value in U.S. yields may be increasing demand from foreign investors, as interest rates in many major economies are near zero or even negative. While one must be careful in assuming “this time is different”, the factors above appear credible and shouldn’t be discounted.

Implication for Investors

For investors with a long-term financial plan, much of this discussion amounts to noise. Market developments may be fascinating for those who are interested, but the news flow of the day should not tempt investors into increased portfolio activity. If a perfect and actionable indicator existed, everyone would use it, and everyone would be rich. Alas, this is simply not the case. Despite being one of the best precursors of trouble, there remains significant uncertainty following an inversion. A false positive is always a possibility, and there are some credible guesses as to why that could be the case now. Furthermore, even if a recession is coming, there is a massive range of outcomes in terms of time till recession and stock market performance that can result.

Maintaining a balanced and diversified portfolio frees the investor from trying to see into the future. If your portfolio remains appropriate relative to your financial plan, an inversion (or any other market development) should not be the catalyst for change. Diversified portfolios are designed with the knowledge that the market is cyclical, and that recessions are inevitable. What investors SHOULD do, however, is use the inversion as a sign to recalibrate expectations. Prepare yourself mentally for the possibility the road ahead will be bumpier. Those that stick to their plan in the face of fear and uncertainty have historically been rewarded.

- Competition, Achiever, Relator, Analytical, Ideation

Josh Jenkins, CFA

Josh Jenkins, Chief Investment Officer, began his career in 2010. With a background in investment analysis and portfolio management from his previous roles, he quickly advanced to his current leadership position. As a member of the Lutz Financial Board and Chair of the Investment Committee, he guides Lutz Financial’s investment strategy and helps to manage day-to-day operations.

Leading the investment team, Josh directs research initiatives, while overseeing asset allocation, fund selection, portfolio management, and trading. He authors the weekly Financial Market Update, providing clients with timely insights on market conditions and economic trends. Josh values the analytical nature of his work and the opportunity to collaborate with talented colleagues while continuously expanding his knowledge of the financial markets.

At Lutz, Josh exemplifies the firm’s commitment to maintaining discipline and helping clients navigate market uncertainties with confidence. While staying true to the systematic investment process, he works to keep clients' long-term financial goals at the center of his decision-making.

Josh lives in Omaha, NE. Outside the office, he likes to stay active, travel, and play golf.

Recent News & Insights

Lutz Named Gold Winner in Quantum Workplace's 2025 Employee Voice Award

Update: Tax Highlights of “The One, Big, Beautiful Bill”

From Seed to Scale: Tax & Operational Strategies for AgTech Startups

Case Study: A Smarter 401(k) Strategy for a Busy Doctor's Office